Perovskite Solar Cell Efficiency: The global push toward decarbonisation and renewable energy growth has placed the solar photovoltaic (PV) sector at the forefront of the energy transition. Among various PV technologies, a newer class — perovskite solar cells — is rapidly gaining attention. Their promise: higher efficiencies, lower cost manufacturing, flexible form factors, tandem‐stack options, and new market opportunities. But as with any emerging technology, there are critical questions around stability, scalability, commercial readiness and, of course, investment attractiveness.

This article explores the intersection of solar cell efficiency in the perovskite domain and the investment dynamics that are following it. We will examine the current state of perovskite cell efficiencies, the key challenges to commercial adoption, the market and investment landscape, and what this means for investors, manufacturers and the broader solar ecosystem.

What are Perovskite Solar Cells?

The term “perovskite” refers to a class of materials that adopt the same crystal structure as the mineral perovskite (calcium titanium oxide, CaTiO₃). In the context of solar cells, “perovskite” usually refers to metal-halide perovskites (for example methylammonium-lead-iodide, CH₃NH₃PbI₃), which have favourable semiconductor properties: direct band gaps, high absorption coefficients, tunable bandgaps, and relatively simple solution‐processing routes.

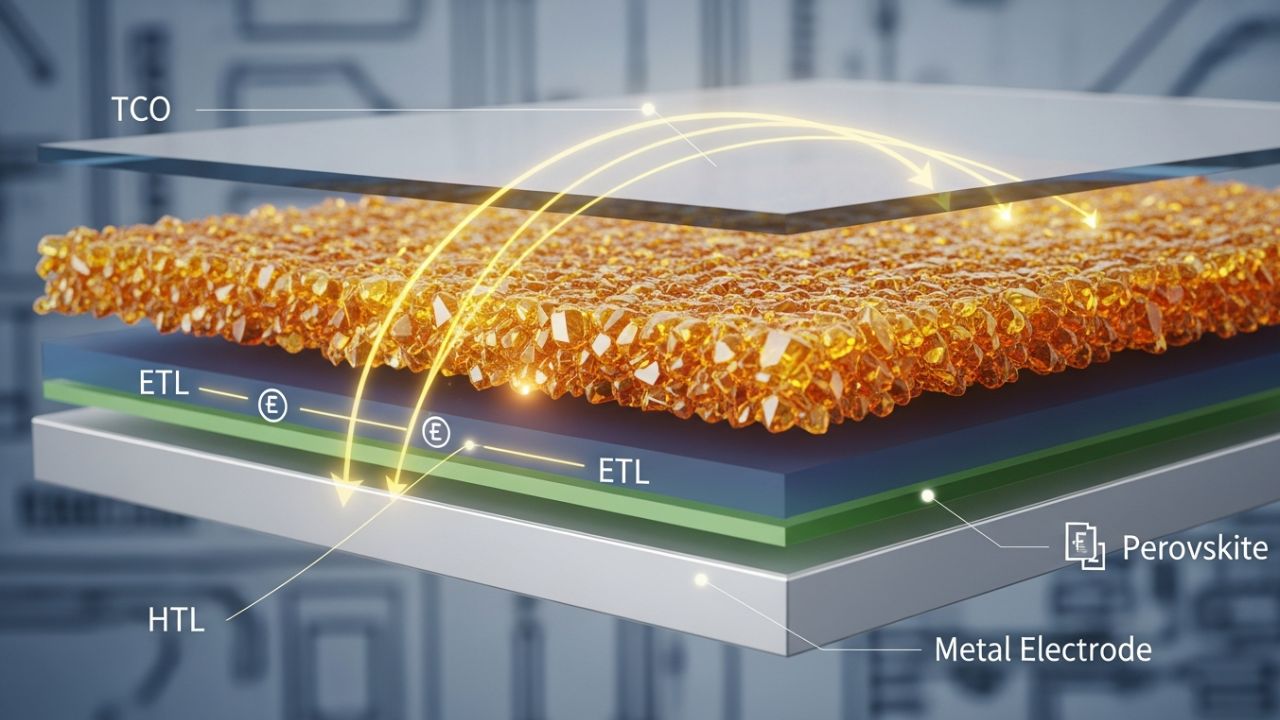

The basic architecture of a perovskite solar cell involves a perovskite absorber layer sandwiched between an electron-transport layer (ETL) and a hole-transport layer (HTL), with metal contacts to extract current. energy.gov One of the big advantages is the potential for low-temperature processing, printable or roll-to-roll manufacturing, and thin-film flexibility – all of which could reduce costs compared to traditional silicon PV.

However, the road to commercialisation has to overcome hurdles: long-term stability (e.g., moisture, ion migration, thermal/UV degradation), scaling from small cells to large modules, encapsulation, and achieving reliability tantamount to the decades-long lifetime of silicon panels.

Efficiency Achievements: How Far Has Perovskite Come?

Efficiency — typically expressed as power conversion efficiency (PCE) — is a core metric. Let’s examine where perovskite technology stands, and what that implies for investment.

Single-junction perovskite cells

In the early days (~2009) perovskite solar cells had efficiencies of just a few percent. According to the U.S. Department of Energy (DOE), perovskites progressed from about 3% in 2009 to over 26% for small area devices. More recently:

- A 2023 achievement by the National University of Singapore (NUS) team reported a stabilised efficiency of 24.35% on a 1 cm² active area device.

- According to a “2025 update” by Fluxim, the certified record for a single-junction perovskite cell stands at 26.7% (device area 0.052 cm²) by the University of Science and Technology of China (USTC).

- There are also consistent reports of ~21.6% efficiency from the Australian National University (ANU) team for a larger-size perovskite cell.

These numbers put perovskite materials in the ballpark of commercial silicon cells, though the challenge remains scaling and ensuring durability.

Tandem perovskite/silicon (and other) architectures

A particularly exciting avenue is tandem cells, where a perovskite layer is stacked on top of a silicon (or other bottom cell) to absorb a broader portion of the solar spectrum. The result: higher theoretical efficiencies than single-junction limits. The DOE notes that perovskite-silicon tandems have reached almost 34%. Specific published record:

- The King Abdullah University of Science and Technology (KAUST) claimed a 33.7% certified efficiency for a 1 cm² perovskite/silicon tandem solar cell.

This places perovskite tandem technology firmly on the radar for next-generation high-efficiency PV modules.

Why do these numbers matter?

Efficiency improvements lead to multiple downstream advantages:

- Lower cost per watt: A higher efficiency cell means fewer panels (less area) for the same output, reducing land, mounting, wiring, BOS (balance-of-system) costs.

- More power from the same footprint: This is especially relevant in rooftop, built-environment, or constrained land applications.

- Competitive edge: As silicon technologies mature, incremental gains become harder; perovskites can offer faster leaps.

- Market differentiation & premium valuations: Investors are more willing to commit capital when there is a credible pathway to higher efficiencies and cost reduction.

The Investment Landscape: Where Capital is Flowing

Given the strong performance trajectory, where is the investment going? And what do these trends signal for potential returns and risks?

Market size and growth forecasts

The market for perovskite solar cells is forecast to grow rapidly:

- According to one estimate, the global perovskite solar cell market size is expected to grow from USD 267.2 million in 2025 to USD 3,604.85 million by 2034, representing a compound annual growth rate (CAGR) of ~34.13%.

- Another source projects the perovskite solar cell market to exceed USD 8.8 billion by 2034, factoring in strong growth in manufacturing capability, government subsidies, and application expansion.

These figures highlight the investment potential — not just in cell manufacture, but in module assembly, tandem integration, system deployment, and associated supply chains.

Investment in R&D, manufacturing, pilot lines

According to Market Growth Reports: between 2022 and 2024, over USD 2.1 billion of commitments have been made globally into pilot production lines, R&D centres and material refinement plants in the perovskite sector.

Geographically:

- Asia-Pacific leads in infrastructure funding (e.g. China allocating large sums to domestic perovskite manufacturing).

- Europe has state-backed programs; for example Germany allocating €320 million toward tandem module R&D and pilot deployment.

- In the U.S., the DOE’s “Solar Energy Technologies Office” (SETO) is funding thin‐film PV including perovskites, signaling government support.

Key investment themes and opportunities

Several investment themes emerge:

- Cell materials & interface engineering: Because perovskite performance depends heavily on defect passivation, interlayer tuning, transport layers, and stability engineering, many startups focus on novel materials.

- Tandem integration: The perovskite–silicon or perovskite–perovskite tandem market is considered where the “leap” in performance lies. Early entrants that can scale may command premium valuations.

- Manufacturing scaling & modules: Moving from lab‐scale (cm²) devices to full‐size modules is challenging. Investments into pilot lines, module encapsulation, reliability testing are critical.

- Supply chain & manufacturing equipment: Because perovskite production may allow lower‐temperature, printable processes, equipment vendors and material suppliers are potential beneficiaries.

- Commercial deployment & early adopters: Rooftop, building‐integrated PV (BIPV), flexible solar, or specialty markets (e.g., portable/indoor) may adopt perovskites earlier and offer investors a stepping‐stone to large utility markets.

- Regional manufacturing hubs: Because solar manufacturing is capital-intensive and often incentivised by governments, there is opportunity in geographic advantage (e.g., China, India, US, Taiwan).

Risks and what investors must watch

While the potential is high, perovskite investments carry unique risks:

- Stability & lifetime: Commercial PV panels need 20-25 year lifetimes, and perovskites still face durability concerns (moisture, UV, heat, ion migration). Many lab cells show strong initial efficiency but may degrade quickly.

- Scalability: Achieving >25% efficiency in a 0.05 cm² cell is one thing; scaling that to modules (1000s of cm²) with minimal drop is another.

- Commercial readiness & certification: Standards, certification, warranties, bankability – investors will want proof that perovskite modules can perform under real-world conditions.

- Competition: Silicon PV continues to improve (and cost continues to fall). Other technologies (e.g., heterojunction, TOPCon, thin-film) also compete.

- Manufacturing hazards: Many current perovskites use lead – environmental/regulatory pressures may arise. Material supply or processing defects may hamper yields.

- Intellectual property & manufacturing “moats”: Because many materials/processes are academic, translating to manufacturing scale and protecting IP is complex.

- Market timing: If commercialisation takes too long, early investors may face incumbent solar oversupply or commoditised market pricing.

Read Also:Solar Panel Installation Near Me in Chennai

Why Perovskite Efficiency Gains Matter for Investment

Let’s unpack precisely why efficiency gains in perovskite solar cells are central to the investment thesis.

Lower cost per watt, faster ROI

Efficiency improvements directly drive lower levelised cost of electricity (LCOE). For an investor, that means better margins, shorter payback periods, and more compelling project economics. Consider: if a new cell offers 30% efficiency and can be manufactured at comparable cost to a 20% silicon cell, the cost per watt drops significantly. That makes solar projects more bankable and attractive.

Accelerated value chain opportunities

When a disruptive technology improves efficiency rapidly, it often accelerates the value chain: module manufacturers, BOS suppliers, installers, project developers all stand to benefit. For example: if perovskite-silicon tandem modules can reach 30–35% efficiency, installations may require less area, less mounting hardware, less land – reducing soft costs. That opens investment in system integration, real-estate constrained projects (e.g., urban rooftops), BIPV, and offshore floating PV.

Strategic positioning & first‐mover advantage

In any technology shift, early movers capture outsized value. If a company or region positions itself early in perovskite manufacturing, it may gain market share, IP leadership, and cost advantages. For example, companies pursuing tandem cells or high‐throughput printable perovskite modules may command premium valuations. This dynamic attracts venture capital, private equity and strategic corporate investment.

Broadening application space

Perovskite’s flexibility (thin film, lightweight, colour‐tunable, semi‐transparent) expands application beyond conventional rigid modules. That means new markets: building-integrated photovoltaics (windows, façades), portable solar, indoor ambient light harvesting, off‐grid microgrids, electric vehicle integration. For investors, diversification of addressable market means risk mitigation and multi‐path revenue models.

Government incentives & policy tailwinds

Because perovskite technologies align with decarbonisation, renewable energy targets, and manufacturing sovereignty agendas (especially in mature economies), they benefit from subsidies, grants, research funding, and preferential regulatory regimes. That de-risks investment somewhat and may improve returns. For example, the DOE in the U.S. funds perovskite R&D.

From Lab to Marketplace: Key Performance and Commercialisation Metrics

It’s useful to understand how efficiency numbers translate—and what else needs to be addressed for commercial viability.

1. Cell vs. module vs. system efficiency

- Cell efficiency: Measured on small area devices (typically <1 cm²) under standard test conditions. Achieving high values here is a strong indicator.

- Module efficiency: When cells are scaled and assembled into modules (hundreds to thousands of cm²), the efficiency usually drops due to interconnects, shading, mismatch, edge losses, temperature.

- System efficiency/LCOE: Ultimately modules are part of a full system with wiring losses, inverter efficiency, soiling, degradation over time; for investors, the system performance and economics matter most.

Thus, when a research team announces a 26% cell efficiency, investors should dig deeper: what is module efficiency, what is degradation over time, what is reliability under field conditions?

2. Stability, degradation, durability

High initial efficiency is necessary but not sufficient. For commercial modules, lifetimes of 20-25 years are expected, with warranties typically guaranteeing ~80% of rated output at year 25. Perovskites must show minimal performance loss over time, under thermal cycles, humidity, UV exposure, mechanical stress.

For instance: research at Oxford University and others demonstrated improved heat-stability perovskite cells retaining 95% of initial 24.3% efficiency after 1,000 h in damp‐heat tests. The American Ceramic Society That is encouraging but still not matching typical 20+ year field performance.

3. Scalability and manufacturability

Many high efficiency results are on tiny devices (cm² or less). Scaling to full-size modules (e.g., 1 m² or larger) introduces new defects, uniformity issues, yield losses, encapsulation challenges, material supply issues. For example, a cell of 0.05 cm² with 26.7% efficiency is impressive but says less about manufacturable modules.

Manufacturability also involves cost of materials, throughput, process complexity, equipment capital expenditure, yield losses — all of which matter for investor returns.

4. Certification, standardisation, bankability

For large‐scale deployment and project finance, modules must pass third-party certification, field testing, durability standards (e.g., IEC 61215). Bankability (i.e., developers able to receive financing, insurers confident in lifetime) is critical. Early perovskite modules are still on the path toward full bankability, so investment may carry higher risk than established silicon.

5. Supply-chain, materials and IP

Perovskite materials often contain lead (Pb), raising environmental disposal/regulatory concerns. Alternative compositions (tin-based, lead-free) are in development but currently have lower efficiency. Material supply, sourcing, toxicity and recycling strategies are all essential for commercial-scale investment.

Protecting intellectual property and manufacturing process know-how gives competitive advantage; however, many perovskite innovations originate in academia, and the path to industrialisation involves significant technical and business risk.

Read Also: Solar EV Roads: Charging Electric Cars While You Drive

Investment Case: Why Now is Interesting (and Why Caution is Warranted)

Here’s a breakdown of the investment case — both the opportunities and the caveats.

Why interest is high

- Strong efficiency trajectory: Rapid improvement from a few percent at inception to >25% in a decade is rare in solar technologies; this suggests strong R&D momentum.

- Cost reduction potential: Lower temperature, lighter weight, printable routes promise lower manufacturing cost and new markets (flexible, building-integrated, portable).

- Tandem growth path: Perovskite-silicon, perovskite-perovskite tandems can unlock efficiencies significantly above single-junction limits (30-35%+), providing a clear path to differentiation.

- Market expansion: With the solar market continuing to grow (driven by decarbonisation, electrification, energy security) perovskites offer a way to tap next-generation PV modules.

- Policy support: Governments around the world are funding thin‐film PV and manufacturing sovereignty initiatives — perovskites benefit.

- Valuable IP and early mover advantage: Investing early in perovskite manufacturing or module businesses may capture outsized upside if commercialisation succeeds

Why caution is necessary

- Commercial risk: Many efficiency claims are lab-scale; full commercialisation (modules, manufacturing, deployment) still has unanswered questions.

- Durability/lifetime risk: If modules degrade rapidly or cannot match silicon’s 20-25 year life, the business model is undermined.

- Scaling/manufacturing risk: Process, yield, supply chain issues may delay or increase costs unexpectedly.

- Competitive pressure: Silicon PV remains dominant, and module costs continue to fall. A perovskite business must show clear cost and performance advantage to gain share.

- Regulatory/environmental risk: Materials (lead, etc) and manufacturing waste/disposal considerations may raise costs or regulatory burdens.

- Timing & market adoption risk: If commercialisation takes too long, the window of opportunity may narrow or incumbents may adapt.

What Does This All Mean for Stakeholders?

For investors (venture capital, private equity, public markets)

- Stage differentiation: Early-stage startups (materials, novel transport layers) carry high risk/high reward. Later-stage module or manufacturing companies may offer more stable albeit lower upside.

- Due diligence focus: Investors should look for validated efficiency (certified data), scale demonstration (pilot modules), lifetime/durability testing, supply-chain readiness, manufacturing cost modelling, competitive differentiation.

- Portfolio diversification: Because uncertainty remains high, perovskite investments may best be part of a broader renewable energy/solar portfolio, rather than a single “bet-the-farm” play.

- Exit pathways: Strategic acquirers (large solar module manufacturers, utility companies) may buy perovskite firms once technology risk reduces. Patents, manufacturing know-how, or first-mover modules can be attractive M&A targets.

For manufacturing companies & module makers

- Consider joint ventures or partnerships to access perovskite/tandem know-how.

- Pilot production lines now, even if small scale, help capture manufacturing learning curves.

- Maintain risk mitigation by preserving silicon backup paths while evaluating perovskite integration.

- Monitor certification regimes and early commercial module deployments to de-risk market entry.

For project developers & utilities

- Keep an eye on emerging perovskite module availability; while mainstream rollout may still be a few years away, early pilot deployments may offer value.

- Evaluate whether perovskite modules (if mature) can deliver lower LCOE or reduced BOS costs owing to higher efficiency and/or flexible form factors.

- Consider applications where higher efficiency or lighter weight matter: rooftops with limited area, BIPV, floating PV, or portable/off-grid systems.

For policy makers & governments

- Support R&D and pilot manufacturing to capture domestic manufacturing value in perovskite supply chain.

- Ensure regulatory frameworks address new materials (lead, tin, recycling) to enable safe scale-up.

- Incorporate perovskite modules into incentive/regulatory regimes once bankability and certification are proven.

Case Study: Efficiency Milestones and Investment Signals

Here are a few key milestones which show how efficiency breakthroughs correlate with investment signals and commercial impetus:

- June 2023 – NUS team records 24.35% for 1 cm² perovskite cell. This signalled that perovskite was closing the gap with silicon in single-junction performance.

- 2023 – KAUST reports 33.7% for perovskite/silicon tandem. pv magazine India That opened the possibility of next-gen tandem modules. Reports of state-backed manufacturing plans followed.

- Market forecasts (2025-2034) show ~30%+ CAGR in perovskite market value.

- Investment data – USD 2.1 billion between 2022-2024 committed globally to perovskite cell/manufacturing initiatives.

Each of these shows how technological progress triggers investment momentum. But note that commercial deployment lags lab records by months/years; investors must bridge this “valley of death” between R&D and mass manufacture.

Specific Considerations for India and Emerging Markets

Given your location in Erode, Tamil Nadu, India, it’s useful to reflect on how perovskite investments might play out in the Indian and emerging-market context.

India’s solar ambitions & the implication

India has ambitious solar energy targets (hundreds of gigawatts), and domestic manufacturing is a strategic policy area (for jobs, supply security, import substitution). A perovskite manufacturing ecosystem offers potential: lower‐cost, flexible modules, manufacturing localisation, and export opportunities.

Localization risks and opportunities

- Opportunity: Roof-top solar in India faces land/space constraints; higher‐efficiency perovskite modules could be a strong value proposition.

- Manufacturing: Tamil Nadu has industrial infrastructure and skilled labour; a hub for perovskite manufacturing could align with state policy.

- Cost sensitivity: Emerging markets are cost-sensitive; if perovskite modules can undercut silicon with higher efficiency, they may gain traction faster.

- Durability in local climate: India’s ambient conditions (heat, humidity, dust) present a durability test — modules need to meet these challenges for local acceptance.

- Import vs. local manufacturing: Trade policy, tariffs, Subsidy regimes will influence whether perovskite modules are imported or locally manufactured; local manufacturing would add jobs and value.

Investor viewpoint in India

- Track early pilot deployments in India of perovskite modules.

- Monitor policy support (government grants, incentives) for advanced photovoltaic manufacturing.

- Consider joint ventures or collaborations between Indian manufacturers and perovskite technology developers.

- Evaluate risk of technology adoption: while mainstream silicon supply chains are well-established, perovskite remains an early technology — time to entry matters.

What to Watch: Key Metrics and Milestones for Investors

If you’re considering the perovskite solar cell space from an investment or strategic perspective, here are key metrics and milestones to track.

- Certified efficiency records: For cell, module, and system levels; and performance under real-world conditions.

- Module efficiency at commercial scale: e.g., >25% module efficiency with size >0.1 m² as a threshold moving toward production readiness.

- Manufacturing pilot lines: Year of first production, throughput (MW or GW), yield, cost per watt of manufacturing.

- Stability/durability data: 1,000+ hours damp-heat tests, thermal cycling, UV exposure, T80 or T90 lifetime predictions.

- Cost per watt comparisons: Manufacturing cost, balance‐of‐system cost, installation cost vs. silicon equivalents.

- Market adoption/early deployments: Signed offtake agreements, reference projects, module availability in the market, warranties offered.

- Supply-chain development: Materials sourcing (e.g., precursor chemicals, lead-free alternatives), manufacturing equipment vendors, local/regional manufacturing ecosystem.

- Regulatory and certification status: Inclusion of perovskite modules in standard certification bodies, warranties, insurance acceptance.

- Investment and M&A activity: Amount of capital committed to perovskite businesses, acquisitions by major solar firms, strategic partnerships.

- Regional manufacturing policy and incentives: Government subsidies, manufacturing incentives, import tariffs, localisation mandates.

Outlook: Where Could Perovskite Go from Here?

Based on current trajectories, here’s how I see the next 5–10 years unfolding for perovskite solar cells — and what that implies for investors.

Near‐term (1-3 years)

- More pilot production lines emerge; module efficiency climbs into the low 20%+ range for larger modules.

- First commercial perovskite modules launched, likely for niche markets (rooftop, flexible, BIPV) rather than utility-scale.

- Tandem modules (perovskite + silicon) may begin limited commercial demonstration.

- Investment continues in manufacturing scale-up, equipment, supply-chain localisation.

- Investors will see clearer data on durability and field performance; companies that provide credible warranties will lead.

Medium‐term (3-7 years)

- If stability and manufacturing yield are proven, perovskite modules could compete directly with silicon in cost-performance.

- Tandem modules may reach 30-35% efficiency in commercial modules, offering significant advantage and gaining market share.

- Large-scale deployment starts in utility-scale projects as well as rooftop/BIPV.

- China, India, USA, EU compete in manufacturing; cost per watt may fall rapidly as learning curves kick in.

- Consolidation in the industry: acquisitions, mergers as larger firms integrate perovskite capability.

Long-term (7-10+ years)

- Perovskite becomes mainstream alongside (or even replacing) some silicon deployments, especially where high efficiency, lightweight, flexible, or integrated installations matter.

- Manufacturing cost per watt converges with or undercuts mature silicon modules; perovskite manufacturing becomes high-volume, low‐cost.

- Recycling, materials sustainability, lead‐free alternatives become standard; supply-chain mature.

- Global market share of perovskite (and tandem) modules becomes significant (e.g., >20-30% of new PV installations).

- Emerging markets adopt perovskite modules for off-grid and distributed solar given their cost and efficiency advantages.

Potential game-changers

- A credible 20+ year lifetime warranty for perovskite modules would shift market commitment.

- Commercial manufacturing of >GW scale perovskite module lines with cost per watt below silicon would accelerate adoption.

- Discovery of a low-cost, lead-free perovskite chemistry with similar efficiency and durability would reduce regulatory and environmental risk.

- Regulatory or import tariff changes favour domestic perovskite manufacturing in major regions (India’s Make in India, US IRA incentives, EU Critical Raw Material strategy).

Conclusion

The technology of perovskite solar cells represents one of the most dynamic and promising fronts in the photovoltaic industry. With efficiency climbing rapidly—from a few percent in the early days to over 26% for single-junction cells and more than 33% for tandem cells—the performance piece is being convincingly established.

For investors, the rationale is compelling: higher efficiencies, potential cost reduction, new markets (BIPV, lightweight/flexible modules), and policy tailwinds. The forecasts reflect this: a market growing at ~30%+ CAGR, with the potential to reach billions in value by 2030 +.

However, the caution cannot be ignored. Many of the highest efficiency cells remain at lab scale; commercial manufacturing, module durability, supply-chain maturity, and field performance remain hurdles. For those investing today, the key is selectivity: backing companies with credible roadmap to manufacturability and durability, watching for milestones, and partnering with manufacturing and deployment ecosystems.

In the Indian context, where solar deployment is accelerating and manufacturing localisation is a policy priority, perovskite technology offers a strategic opportunity — especially if manufacturing can be localised, cost curves can be driven down, and modules adapted to local climatic conditions.

To summarise: efficiency gains in perovskite solar cells are not just academic curiosities—they are the gateway to commercial breakthroughs, which in turn drive investment opportunities. For investors, the time to watch closely is now: technology curves are steep, market openness is increasing, and the next few years may determine which companies, regions and technologies become dominant in the next solar era.

Related Posts

1 thought on “Perovskite Solar Cell Efficiency: The Future of Solar Energy and Smart Investment Opportunities”