Residential Solar Financing Options USA: Switching to solar energy is one of the smartest financial and environmental decisions a homeowner can make today. However, one of the biggest concerns people face is how to afford the upfront cost of installing solar panels. The good news is that residential solar has become more accessible than ever, thanks to a wide range of financing options designed to suit different budgets and financial goals.

In this comprehensive guide, you’ll discover everything you need to know about residential solar financing options in the USA, including loans, leases, power purchase agreements (PPAs), incentives, and expert strategies to maximize your return on investment.

Why Solar Financing Matters More Than Ever

The average cost of a residential solar system in the U.S. ranges between $15,000 and $30,000, depending on system size and location. While this may seem expensive, financing options allow homeowners to install solar with little to no upfront cost.

Solar financing is important because it:

- Makes solar accessible to a wider audience

- Helps homeowners start saving immediately

- Spreads the cost over manageable monthly payments

- Enables faster adoption of clean energy

With rising electricity prices and strong government incentives, financing solar is no longer a burden—it’s a strategic financial decision.

Read Also: Commercial Solar Panel Installation USA: Costs, Benefits & ROI Guide 2026

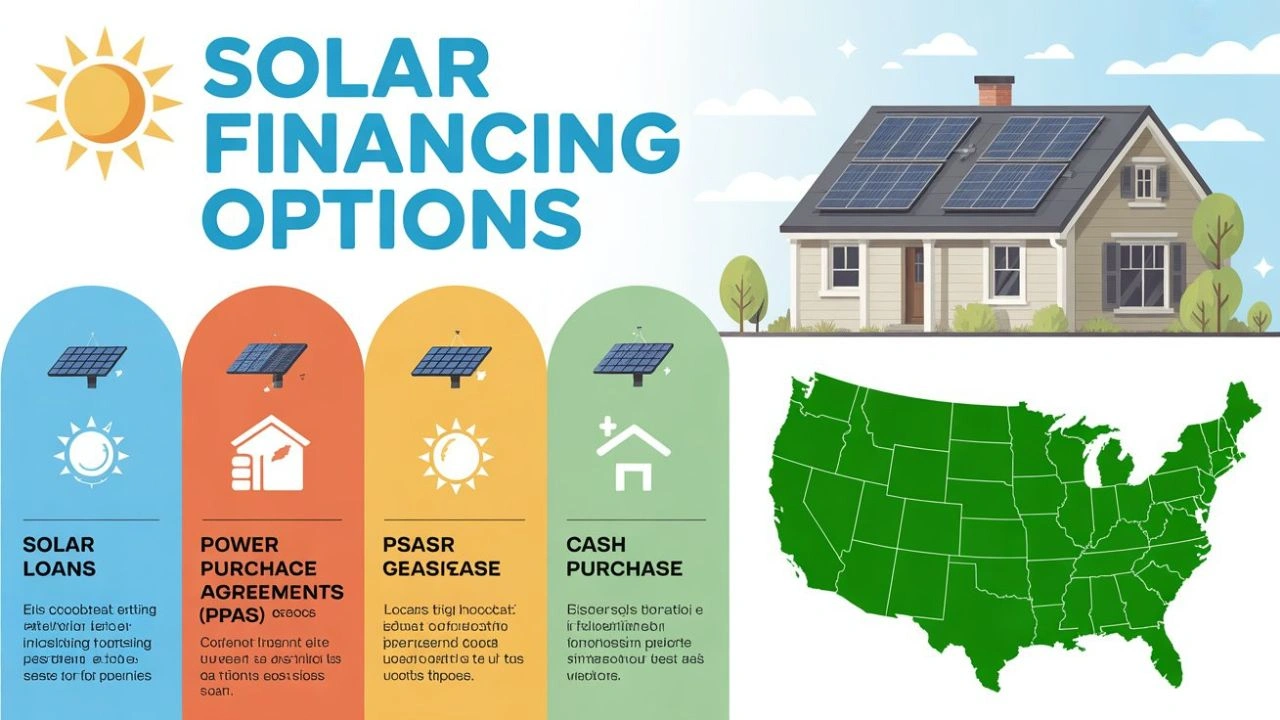

Overview of Residential Solar Financing Options

There are four primary ways to finance a solar system:

- Cash Purchase

- Solar Loans

- Solar Lease

- Power Purchase Agreement (PPA)

Each option has its own advantages and drawbacks, and choosing the right one depends on your financial situation, long-term goals, and tax eligibility.

Cash Purchase: Maximum Savings and Full Ownership

Paying for solar upfront in cash is the simplest and most profitable option.

Key Benefits

- Highest long-term savings

- Immediate ownership of the system

- Eligibility for all tax credits and incentives

- No monthly payments or interest

Drawbacks

- High upfront cost

- Reduced liquidity

Best For

Homeowners who have sufficient savings and want to maximize ROI and long-term benefits.

💡 Expert Insight: A cash purchase typically delivers the fastest payback period, often within 4–6 years.

Solar Loans: Affordable Ownership with Flexible Payments

Solar loans are one of the most popular financing options in the U.S. They allow homeowners to install solar with little or no upfront cost while still owning the system.

Types of Solar Loans

Secured Loans (Home Equity Loans)

- Lower interest rates

- Use your home as collateral

Unsecured Loans

- No collateral required

- Slightly higher interest rates

Key Benefits

- Ownership of the system

- Eligibility for tax credits

- Flexible repayment terms (5–25 years)

Drawbacks

- Monthly loan payments

- Interest costs

Best For

Homeowners who want the benefits of ownership without paying upfront.

💡 Pro Tip: Choose a loan where monthly payments are equal to or lower than your electricity bill savings.

Solar Lease: Low Upfront Cost, Limited Ownership

A solar lease allows you to use a solar system without owning it. Instead, you pay a fixed monthly fee to the solar company.

How It Works

- The solar company installs and owns the system

- You pay a fixed monthly lease payment

- Maintenance is handled by the provider

Key Benefits

- No upfront cost

- Predictable monthly payments

- Maintenance included

Drawbacks

- No ownership

- Not eligible for tax credits

- Lower long-term savings

Best For

Homeowners who want hassle-free solar with minimal financial commitment.

Power Purchase Agreement (PPA): Pay for What You Use

A PPA is similar to a lease, but instead of paying a fixed monthly fee, you pay for the electricity generated by the system.

How It Works

- Solar company installs and owns the system

- You pay per kWh of electricity used

- Rates are usually lower than utility prices

Key Benefits

- Zero upfront cost

- Immediate savings on electricity bills

- Performance-based pricing

Drawbacks

- No ownership

- Variable payments

- Long-term contracts (20–25 years)

Best For

Homeowners who want to save on energy bills without investing upfront.

Comparing Solar Financing Options

| Feature | Cash Purchase | Solar Loan | Lease | PPA |

| Ownership | Yes | Yes | No | No |

| Upfront Cost | High | Low | None | None |

| Monthly Payment | None | Yes | Yes | Yes |

| Tax Benefits | Yes | Yes | No | No |

| Long-Term Savings | Highest | High | Moderate | Moderate |

Federal and State Incentives That Reduce Costs

Financing becomes even more attractive when combined with government incentives.

Federal Investment Tax Credit (ITC)

- Offers 30% tax credit on system cost

- Available for purchased systems (cash or loan)

State Incentives

Depending on your state, you may receive:

- Cash rebates

- Net metering benefits

- Solar Renewable Energy Credits (SRECs)

Net Metering

Allows homeowners to:

- Sell excess electricity back to the grid

- Offset electricity bills

💡 Important: Incentives can reduce your total cost by 30%–50% or more.

How to Choose the Best Financing Option

Selecting the right financing method depends on your priorities.

1. Choose Cash If:

- You want maximum savings

- You can afford upfront costs

2. Choose a Loan If:

- You want ownership

- You prefer manageable payments

3. Choose Lease or PPA If:

- You want zero upfront cost

- You prefer convenience over ownership

💡 Expert Tip: Always calculate your total lifetime savings, not just monthly costs.

Real Cost Example: Financing a Solar System

Let’s consider a $20,000 solar system:

With ITC (30%)

- Tax credit: $6,000

- Net cost: $14,000

Loan Example

- Monthly payment: ~$120

- Electricity savings: ~$150

👉 Net monthly benefit: $30 savings

Lease/PPA Example

- Monthly payment: ~$100

- Savings: ~$20–$40

Hidden Costs to Watch Out For

While financing solar is beneficial, be aware of:

- Dealer fees

- High interest rates

- Escalation clauses (in leases/PPAs)

- Early termination fees

👉 Always read the contract carefully before signing.

Common Mistakes to Avoid

- Choosing based only on low monthly payments

- Ignoring tax credit eligibility

- Not comparing multiple financing options

- Overlooking system quality

A poor financing decision can reduce your savings significantly.

Future Trends in Solar Financing

The solar financing landscape is evolving rapidly.

Emerging Trends

- Zero-interest solar loans

- Subscription-based solar models

- Integration with smart home financing

- Increased battery financing options

Battery Financing Growth

More homeowners are financing solar batteries to:

- Store excess energy

- Achieve energy independence

- Protect against outages

Read Also: Best Solar Companies Near Me USA 2026 – Top Installers, Costs & Expert Guide

Benefits of Financing Solar Instead of Paying Utility Bills

Many homeowners don’t realize that financing solar can be cheaper than paying utility bills.

Key Advantages

- Fixed monthly payments

- Protection from rising electricity costs

- Long-term savings

- Increased home value

💡 Think of solar financing as replacing your electricity bill with an investment.

Conclusion: Making Solar Affordable for Every Home

Residential solar financing has made clean energy accessible to millions of homeowners across the United States. Whether you choose a cash purchase, loan, lease, or PPA, each option offers a pathway to lower energy costs, sustainability, and energy independence.

The key is to:

✔ Understand your financial goals

✔ Compare multiple options

✔ Work with a trusted solar provider

With the right financing strategy, solar is not just affordable—it becomes one of the smartest long-term investments you can make for your home.

Related Posts